Buying your first home from a mortgage company in Roseville, CA, is a major milestone, but it can also be confusing. While first time home buyer loans are designed to help make things easier, not every detail is shared upfront. In the last two years, first time home buyer household income has grown by twenty-six thousand dollars. This year’s report shows that the median household income of first time home buyers reached ninety-seven thousand dollars. That’s a solid starting point, but income alone does not guarantee the best deal or the smoothest experience.

For anyone entering the market, it helps to work with a mortgage company in Roseville, CA that goes beyond the basics. Big Valley Mortgage, for instance, understands that first time buyers need more than just approval. They require comprehensive information, including the minor details that some lenders may overlook. This guide breaks down what really matters.

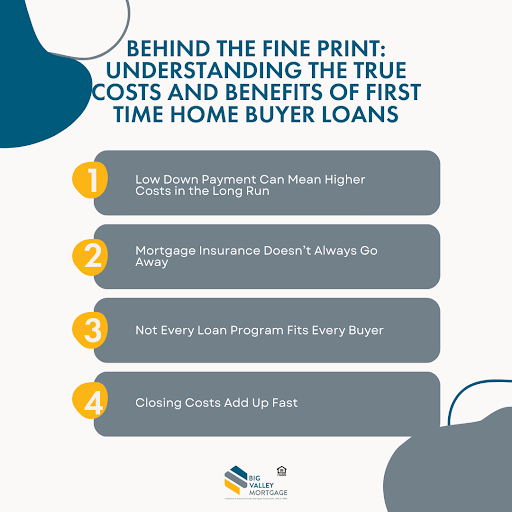

Behind the Fine Print: Understanding the True Costs and Benefits of First Time Home Buyer Loans

Many first time buyer loan programs are marketed as great deals, but the truth is a little more complicated. Here are the things lenders tend to skip over.

1. Low Down Payment Can Mean Higher Costs in the Long Run

Programs that offer down payments as low as three percent are appealing at first. But a smaller down payment often means higher monthly payments. You will also pay more interest over the life of the loan, and you will almost always be required to carry mortgage insurance. That extra insurance cost can add hundreds to your monthly bill and might last for years.

2. Mortgage Insurance Doesn’t Always Go Away

Some loans, like FHA loans, require you to pay mortgage insurance for the full term of the loan, no matter how much equity you build. Conventional loans may let you cancel mortgage insurance once you reach 20 percent equity, but the process takes time and often requires a formal request. This is not something most lenders make clear upfront.

3. Not Every Loan Program Fits Every Buyer

There are many loan types available, and each one is designed for a different situation. For example:

- FHA loans offer flexibility with credit scores but come with long-term insurance costs.

- USDA loans are ideal for rural buyers but have strict location requirements.

- VA loans provide excellent benefits but are only available to eligible veterans.

Choosing the wrong loan could cost you more money or limit your options. A one-size-fits-all approach just does not work.

4. Closing Costs Add Up Fast

Closing costs usually range between two and five percent of the home’s purchase price. For a $400,000 home, that means you might need an extra $8,000 to $20,000 in cash. Lenders sometimes gloss over these details until the final paperwork. Always ask for a complete estimate early so you can plan ahead and avoid surprises.

Mortgage Company in Roseville, CA: What First Time Buyers Should Know Before Choosing a Loan Program

When it comes to choosing a lender, local experience makes a big difference. A mortgage company in Roseville, CA, can offer insights and options that a national chain may not.

1. Local Expertise Can Save You Time and Stress

A mortgage company in Roseville, CA, understands the regional housing market and can match you with programs that make the most sense for your location. They know which neighborhoods qualify for specific assistance programs and how to speed up the approval process based on local regulations.

2. Look for Clarity, Not Just Promises

Avoid lenders who brush over your questions or fill the conversation with complicated terms. A trustworthy lender will explain the real meaning of every rate, fee, and term without making you feel like you need a law degree to understand it.

3. Find a Loan That Works for You

The right lender will listen to your financial goals and help you find a loan that fits, and not just the one they want to sell. This includes helping you understand how to get a mortgage that suits your lifestyle and long-term plans.

Buying your first home is more than a transaction. It is the start of a new chapter. That is why first time home buyer loans deserve more attention than just comparing mortgage rates today. You need to understand the real cost, the loan terms, and how your decision will affect your future.

By working with an experienced mortgage company in Roseville, CA, like Big Valley Mortgage, buyers get the full picture. That means no surprises, no confusion, and no regret after the deal is done.

As housing trends continue to shift, more buyers are stepping into the market. In 2024, seventy-five percent of younger millennials and forty-four percent of older millennials were first time home buyers. If you are ready to be a first time home buyer, make sure you choose a lender who puts your goals first.

Take the first step today. Reach out to the best mortgage company in Roseville, CA, Big Valley Mortgage, and find the loan that fits your life, not just your price range.